BIR RMC 23-2022

21 June 2022 The Bureau of Internal Revenue (BIR) implements Memorandum Circular 23-2022, implements income tax suspension to registered business enterprises still implementing work-from-home (WFH) arrangements.

The Bureau of Internal Revenue (BIR) has issued Revenue Memorandum Circular (RMC) 39-2022, which implements revisions on the payment process for the penalties directed to Registered Business Enterprises (RBEs) in the Information Technology-Business Process Management (IT-BPM) sectors that are in violation of the Work-From-Home (WFH) threshold requirements implemented by the Fiscal Incentives Review Board (FIRB).

This RMC follows the guidelines previously established by BIR RMC 23-2022, which required the suspension of all tax incentives for RBEs operating in IT-BPM sectors if they do not comply with the WFH threshold given by the FIRB. All uncompliant RBEs must pay the regular income tax of 20% or 25% for the months in which the violations have occurred.

Additionally, the RMC explains RBEs that have no current transactions that are subject to regular income tax have the option to pay the penalty by indicating the taxable income under the column “regular” of BIR Form No. 1702-MX. The RBEs with existing transactions subject to the regular income tax must use BIR Form No. 0605 for voluntary payment of penalties.

The revisions of the RMC towards the guidelines are as follows:

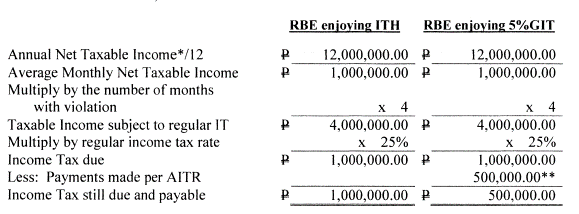

The RMC explains that RBEs will need to compute the penalty using the guidelines given by the circular. The same amount will have to be paid within thirty (30) days after the due date prescribed for the payment of Income Tax. The same administrative penalties will be imposed if the payment is made AFTER the date given since the penalty pertains to ‘Income Tax’. The RMC then states that the penalty must be calculated as follows:

*Assume that the RBE committed violations in September, October, November and December of 2021.

*Annual Taxable Income must be computed based on existing tax laws and policies.

**Assuming the GIT per AITR is PHP 1,500,000 (inclusive of LGU share), the monthly GIT paid is PHP 125,000 multiplied by four months.

21 June 2022 The Bureau of Internal Revenue (BIR) implements Memorandum Circular 23-2022, implements income tax suspension to registered business enterprises still implementing work-from-home (WFH) arrangements.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.