Mandatory Supporting Documents for VAT

Mazars highlights the essential mandatory supporting documents for Value Added Tax (VAT) in the Philippines.

Overview

Value-Added Tax is a form of sale tax which is levied in the sale of goods, services, and importation of goods into the Philippines. The tax rate of 12% may be shifted or shouldered by the end-consumer. Furthermore, a VAT registered person shall issue the following to their customers:

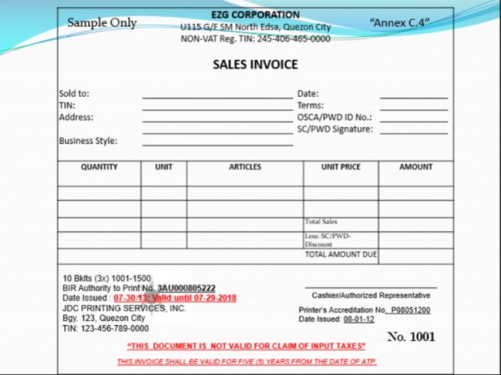

- VAT Sales Invoice– for every sale, barter or exchange of goods or properties. The customer may claim the Input tax whenever the Sales Invoice is already available; and

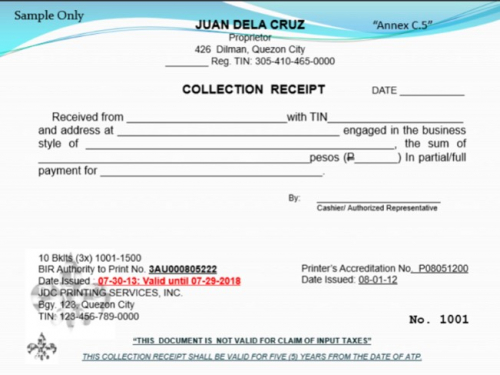

- VAT Official Receipts – for every lease of goods or properties and for every sale, barter or exchange or services. The customer may can claim the Input tax once paid and an Official Receipt is available.

The Revenue Memorandum Order (RMO) 12-2013 mentioned the required information to be indicated on the Official Receipts (ORs), Sales Invoices (SIs) and Other Commercial Invoices (CIs). However, these information are only applicable to the issue of manual SIs, CIs and ORs and excludes taxpayers issuing receipts through Cash-Register Machine/Point-of-Sale Machines (CRM/POS) and the computerized accounting system (CAS).

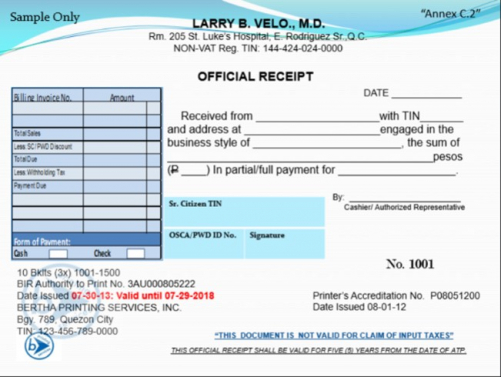

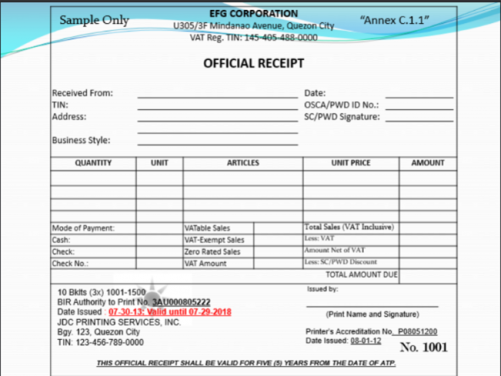

The ORs/SIs/CIs shall be printed showing among others the following:

- Taxpayer’s Registered Name;

- Taxpayer’s Business Name/Style (if any); - Revenue Memorandum Circular 55-2019 to clarify the definition of “Business Style” this refers to the business name registered with the concerned regulatory body used by the taxpayer other than its registered name or company name.

- A statement that the taxpayer is VAT or Non-VAT registered followed by the Taxpayers Identification Number (TIN) and 4-digit Branch Code. (Example: VAT Registered TIN 123-456-789-0000);

- Business address where such ORs/SIs/CIs shall be used;

- Date of transaction;

- Serial number of the OR/SI/CI printed prominently;

- A space provided for the Name, Address and TIN of the buyer;

- Description of the items/goods or nature of service;

- Quantity;

- Unit cost;

- Total cost;

- VAT amount (if transaction is subject to 12% VAT);

- If the VAT taxpayer is engaged in mixed transactions, the amounts involved shall be broken down to: Vatable Sales, VAT Amount, Zero Rated Sales, and VAT Exempt Sales;

- For Non-VAT ORs/SIs, and other CIs (VAT or Non-VAT) such as delivery receipts, order slips, purchase orders, provisional receipts, acknowledgment receipts, collection receipts, credit/debit memo, job orders and other similar documents that form part of the accounting records of the taxpayer and/or issued to their customers, in addition to the above-enumerated applicable information, the phrase “THIS DOCUMENT IS NOT VALID FOR CLAIM OF INPUT TAX” in bold letters, shall be conspicuously printed at the face of the Non VAT ORs/SIs and other CIs;

- Taxpayers whose transactions are not subject to VAT or Percentage Tax shall issue non-VAT principal receipts/invoices indicating prominently at the face of such receipts/invoices the word “EXEMPT”.

- The following information shall be printed at the bottom portion of the OR/SI/CI:

- Name, address and TIN of the accredited printer;

- Accreditation number and the date of accreditation of the accredited printer;

- ATP number, OCN, date issued (mm/dd/yyyy)

- BIR Permit Number (if loose leaf OR/SI/CI);

- Approved inclusive serial numbers of OR/SI/CI;

- Security/Special markings/features of the accredited printer;

- The phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEAR FROM THE DATE OF THE ATP”. This is no longer required to be indicated at the bottom portion of manual or system-generated receipts/invoices and the BIR approved ATP shall valid until full usage of inclusive serial numbers of the supplementary receipts/invoices reflected in the said ATP. (RR No. 6-2022)

Moreover, the Revenue Regulation 16-2018the amended RR No. 10-2015 on the Use of Non-Thermal Paper for All Cash Register Machines (CRMs) / Point of Sales (POS) Machines and Other lnvoice / Receipt Generating Machine / Software. This revenue regulation provided that all tape receipts issued, and the data printed on the tape receipts shall show the information required under Section 5 of RR l-0-201-5, as amended, namely:

- Taxpayer’s (TP) Registered Name;

- TP’s Business Name/style (if any) - Revenue Memorandum Circular 55-2019 to clarify the definition of “Business Style” this refers to the business name registered with the concerned regulatory body used by the taxpayer other than its registered name or company name.

- A statement that the taxpayer is VAT or NON VAT registered followed by the Taxpayers Identification Number (TlN) and 4-digit branch code

- Machine identification Number (MlN);

- Serial number of the CRM/POS machine;

- Detailed business address where such Official Receipts shall be used/located;

- Date of transaction;

- Serial Number of the OR printed prominently;

- A space provided for the Name, Address and TIN of the buyer;

- Description of the nature of service;

- Quantity;

- Unit cost

- Total cost;

- VAT amount (if transaction is subject to 12% VAT);

- lf the VAT taxpayer is engaged in mixed transactions, the amounts involved shall be broken down to: VATable sales, VAT Amount, Zero Rated Sales, and VAT Exempt Sales;

- For Non-VAT ORs, Sales Invoices and Commercial Invoices (VAT or NON-VAT) such as delivery receipts, order slips, purchase orders, provisional receipts, acknowledgment receipts, collection receipts, credit/debit memo, job orders and other similar documents that form part of the accounting records of the taxpayer and/or issued to the customers, the phrase “THIS DOCUMENT lS NOT VALID FOR CLAIM OF INPUT TAX” in bold letters, shall be conspicuously printed at the bottom of the Non VAT ORs/SIs/CIs;

- Taxpayers whose transactions are not subject to VAT or Percentage Tax shall issue Non-VAT principal receipts/invoices indicating prominently at the face of such receipts/invoices the word ‘EXEMPT’;

- The following shall be printed at the bottom portion of the OR:

- address and TIN of the accredited supplier of CRM/POS/Other similar machines/software;

- Accreditation number and the date of accreditation (issued and value until) of the accredited supplier;

In addition, the Revenue Memorandum Circular 64-2015 was issued to reiterate the information reflected on receipts, invoices and other commercial invoices generated from CRM/POS/receipt generating software pursuant to Revenue Regulations (RR) No. 10-2015 and other regulations regarding VAT receipts and invoices. It provides that the following information of the purchaser, customer or client must be indicated on VAT receipts and invoices, in the case of sales amounting to one thousand pesos (P1,000.00) or more and where the sale is made to a VAT registered person:

- Name of purchaser, customer or client,

- Address

- Taxpayer identification Number (TlN); and

- Business style (if any)

See sample OR’s and Invoices below: